Guide to the Pikes Peak Library District Budget

Due to the complex nature of Pikes Peak Library District’s budget, the Library District is providing this guide to help the community better understand the Library’s budgeting process as PPLD is committed to full transparency of the budget and its processes. PPLD is considered a “Library District,” which is a separate legal entity, and was created through Colorado State Statute (C.R.S. 24-90-110) to provide library services within a specific, voter-approved geographic area. The District is an independent, tax-exempt local government entity and is not considered a component unit of any other government entity or municipality, including El Paso County, Colorado, and is financially, managerially, and operationally independent.

Budget Timeline

During the third and fourth quarters of each year, PPLD staff and Leadership Team officially begin to prepare the Library District’s budget for the next year. While the formal work starts in June, the process begins with the new fiscal year.

- January - Staff start to keep track of their expenses and what they need to create a wish list for the next year's budget.

- June - Staff starts to tally their numbers, forecast activities, prepare events and programs, determine the needs of the collection, pinpoint needed repairs and maintenance, identify necessary security upgrades, craft communication and promotional strategies, and establish how they can best meet the needs of the whole community.

- July - Each department submits their budget requests to the Finance Department. It is then reviewed, discussed, and revised by PPLD’s Leadership Team. The budget is updated until the team is ready to present it to the Board of Trustees.

- October - PPLD's Leadership Team presents the preliminary balanced budget per Colorado Revised Statute § 29-1-105.

- December - After answering the Board’s questions and incorporating its suggested revisions, Leadership Team presents the balanced budget to the Board for approval per Local Government Budget Law, § 29-1-108, C.R.S.

Where does the money come from?

Budgets are blueprints that explain where money comes from, how we will use it, and why it matters.

El Paso County is the most populous county in Colorado, containing the second most populous city in the state — Colorado Springs.

El Paso County boasts a population of nearly 750,000, and PPLD’s legal service area covers nearly 700,000 of those individuals, as Security/Widefield is not in PPLD’s official service area. The Library’s legal service area contains roughly 286,000 households, of which 66.7% have an active PPLD library card. The number of library cards increases monthly as more people move to the Pikes Peak region.

What items affect the budget used to serve the people in the community?

Approximately 95% of our budget comes from a portion of collected property tax and specific ownership tax. Based on a diagram from El Paso County’s 2025 Adopted Budget Book, a home with a market value of $500,000 would have paid $3,008.24 in property tax. At a mill levy rate of 3.14 for this property, PPLD would have received $93 of the total property taxes paid, which accounts for 3.11% of the taxes on this property. Using a dollar bill, below is an illustration of just how much PPLD received of the property taxes paid by homeowners in Colorado Springs in 2025.

Mill Levy

The mill levy rate is the percentage of the property taxes the Library receives each year. In 1986, voters approved that PPLD can collect up to 4.000 mills (a mill is a unit of currency representing one one-thousandth of a dollar [$0.001]). However, due to Colorado’s Taxpayer’s Bill of Rights (TABOR) restrictions on growth, if collecting four mills of the property taxes increases PPLD’s income growth by more than the TABOR limits allow, the Library District cannot collect the full amount. Overall in 2025, PPLD assessed a mill levy of 3.14. We issued a temporary credit to be in compliance with our TABOR limit.

Inflation

Like our personal budgets, inflation affects all parts of the District’s budget: from what money the Library receives from property taxes to the costs of programming, books, databases, personnel, benefits, operation costs, and capital projects. The cost of all of these increases each year.

Keeping these items in mind while putting together our budget ensures we can continue to offer great services, materials, technology, and spaces for our patrons.

TABOR - What is it?

Colorado law limits how much tax money the Library can keep.

If local growth would result in the Library District being able to collect an increased amount of property taxes, TABOR requires PPLD to refund any amounts above the limit.

State law caps government entities’ income growth at 5.5% or the Consumer Price Index (whichever is lower) over the previous year. This means that even if property values rise dramatically, the Library District can only collect a maximum of 5.5% more in taxes than it did the prior year.

For example, suppose you are making $100 a week and you get a 25% raise, but the law says it cannot be more than 5.5%, instead of getting the $125 your boss wants to give you, the law limits your weekly salary to only $105.50.

Understanding Library Funds and Funding

Think of PPLD’s funds like different jars of money. Each fund is created with a specific purpose in mind. Currently, the Library has one major fund and several non-major funds. We will focus on the top three funds of PPLD:

General Fund (Major Fund)

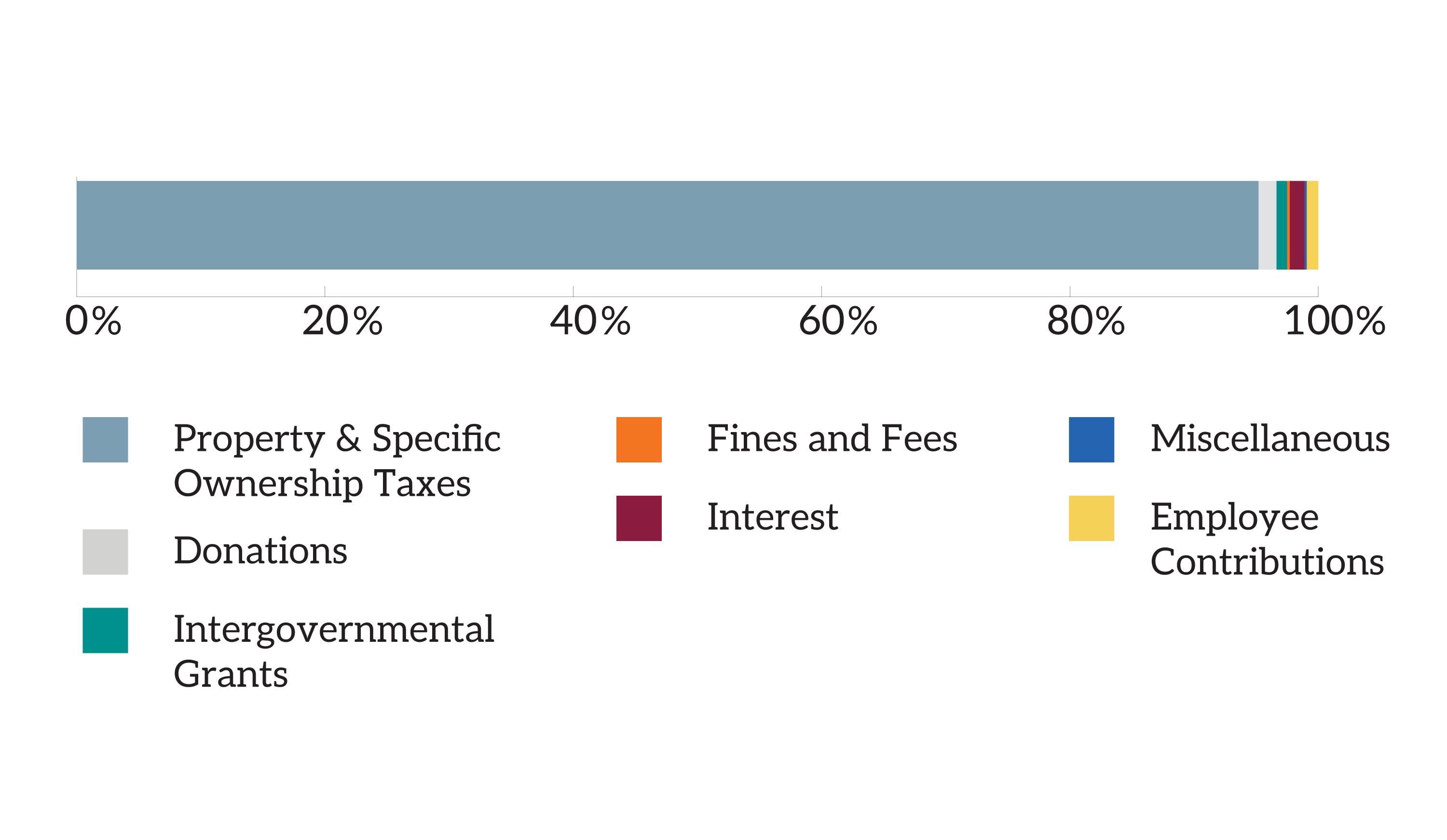

The General Fund is made up of revenue/money we use to support the Library’s daily operations. There are three sources of revenue for the District’s General Fund. The largest portion comes from property taxes and specific ownership taxes (taxes on vehicles such as vehicle registrations) and makes up roughly 95% of the budgeted revenue each year.

The second source of operating revenue consists of revenue from intergovernmental grants, donations through the PPLD Foundation, and miscellaneous revenue generated from fines, fees, paid parking lot collections, and copy and printing fees, contributing 3.8% to the General Fund.

The final revenue source comes from employee contributions toward their health care costs.

Capital Fund (Non-major Fund)

Capital Fund money is set aside for the large, one-time purchases that will last the District a long time, such as buildings, computers, and roofs.

Self-Insurance Fund (Non-major Fund)

The Self-Insurance Fund is a specific fund that is set aside to pay employee health insurance.

| 2025 REVENUES | AMOUNT | % OF FUNDING |

|---|---|---|

| Property & Specific Ownership Taxes | $40,123,322 | 95.19% |

| Donations | $605,000 | 1.44% |

| Intergovernmental Grants | $360,784 | 0.86% |

| Fines and Fees | $90,000 | 0.21% |

| Interest | $500,000 | 1.19% |

| Miscellaneous | $73,962 | 0.18% |

| Employee Contributions | $393,533 | 0.93% |

| TOTAL | $42,146,601 | 100% |

Unassigned Fund Balance

As a government institution, PPLD’s Unassigned Fund Balance refers to the portion of the General Fund that has not been classified as restricted, committed, non-spendable, or assigned for a specific purpose. Below is the breakdown of PPLD’s Unassigned Fund Balance:

| UNASSIGNED FUND BALANCE | |

|---|---|

| End of year 2024 unassigned balance | $18,565,212 |

| (Less) Operating Reserves | ($ 8,376,047)* |

| Remaining Balance Available | $10,189,166 |

| 2025 Capital Fund Spend | ($3,977,745) |

| Other Tax Revenue (SB22-238 and SB23B-001) | ($2,086,606) |

| 2025 AVAILABLE UNASSIGNED FUND BALANCE | $ 4,124,815** |

*The operating reserves included in this chart represent the Board’s mandated three months of reserves to cover PPLD’s operating expenses in the event of an economic crisis.

**The remaining unassigned fund balance for the District in 2025 is $4,124,815. These funds can only be accessed with the approval of the Board of Trustees and are used to cover large purchases, such as building or land purchases. This money is not available to cover operational expenses such as rent, personnel needs, or costs.

How does PPLD Spend Its Money?

Expenses tell you where the Library District spends its revenue and can be broken down into three main categories:

- Personnel - This includes staff salaries and benefits. It makes up the largest category of the Library’s overall budget at 60% and is an ongoing expense.

- Operating expenses - These ongoing expenses make up 31%* of the budget. Items included here are rents, utilities, supplies, software, collection materials (physical materials and eLibrary materials), vehicles, maintenance and building materials, mileage, business memberships, and contract services.

*Due to an inadvertent error, this number was updated Fri., September 26, 2025. - Capital projects - This group makes up 9% of the annual budget and can include upgrades to buildings, parking lots, fences, new equipment, signs, and IT improvements. Capital projects are one-time expenses. For the 2025 budget, PPLD’s Facilities department received $3.1 million, and IT received $866,000 for capital projects.

Here is a 2025 breakdown of PPLD’s expenses:

| EXPENSES | AMOUNT |

|---|---|

| Maintenance | $2,868,485 |

| Capital Funds | $3,977,344 |

| Collection Management Materials | $4,844,359 |

| Contract Services | $2,572,130 |

| Employee Salaries & Benefits | $26,605,518 |

| Mileage, Training, Memberships | $721,630 |

| Programming | $350,390 |

| Telecommunications & Software | $1,236,263 |

| Supplies | $1,207,352 |

| GRAND TOTAL | $44,383,471 |

This guide is meant to be a general overview of PPLD’s budgeting process, providing insight into what affects the amount of money the Library District can receive, as well as an explanation of how the District allocates this money to serve its ever-growing community.

For the complete 2025 budget, visit PPLD’s website at ppld.org/financial-annual-reports